Q4 (Apr-Jun 2022) real GDP growth rate: -0.1% YoY

Q4 real GDP:132 trillion472 billion yen / 1.1% YoY (Source: Cabinet Office)

The market information relating to real estate, which is important when considering the sale or purchase of real estate, has recently reached a major turning point. This year has seen major changes in covid measures and increased economic activity, such as an increase in the number of domestic and international tourists. Many will also focus on the impact of interest rate policy on the property market.

This report provides information on market trends relevant to real estate, based on the latest information available as of August 2022. Hopefully, this will help you to know the best opportunities for buying and selling property.

【1. Upcoming Economic Policy in the Wake of the Reshuffled Second Kishida Cabinet】

The Cabinet was reshuffled on 10 August for the first time since the second Government took office, with 20 members of the Cabinet, including the Prime Minister, being appointed. Of these, 5 remain in office, 9 are first-time cabinet members and 5 are re-appointed. Following this inauguration, Prime Minister Kishida has set the following as his key economic and related policies.

① Implement the Economic Security Promotion Act, prevent the outflow of sensitive technologies and promote supply chain resilience, etc., ② Invest in people (Improve the environment for further wage increases and strengthen various environments such as vocational training), nurture start-ups, green transformation, digital transformation, etc. ③ Explore ways to secure a stable, low-cost energy supply, including through the use of nuclear power; and ④ Strengthen the transition to a new phase of corona countermeasures and response.

It can be said to be in line with the favoured policy approach of the Japan Federation of Economic Organisations (Nippon Keidanren), commonly known as Keidanren, an economic and interest group that is made up mainly of major Japanese companies and retains significant influence in the political arena, which stated on 10 August: 'Giving the fact that the new cabinet is composed of a number of outstanding policy experts, and that it will be able to make the best use of its expertise and experience in the field, will be an important factor in the success of the government's policy. I would like to commend the new cabinet as an extremely strong line-up that is expected to unite the government and ruling party, including LDP officers, to swiftly implement its policies". It is noteworthy that, amongst other things, the government has emphasised the importance of continuing to encourage the government to work on raising wages and improving overall working environments from the perspective of 'investment in people' and 'appropriate distribution to workers', while adhering to the Basic Principles for Wage Determination.

There are many concerns about stagflation, meaning a situation where prices continue to rise despite economic stagnation, as resource and food prices continue to soar and wage increases have not been positive. The Government is expected to take serious measures to combat this, with a focus on policies related to raising wages.

【2.Property Market Related Information: Basic Data on a Real Economy】

According to Table 1 in the following section, the number of new housing starts fell sharply in May (-4.3%) and again in June (-2.2%), although the year-on-year decline narrowed, with the June statistics showing the second lowest level in the past decade. This was partly due to fewer opportunities for business negotiations following the spread of new covid cases, which increased at the beginning of the year. Table 2 also confirms the decline in the number of units supplied. In addition to the decrease in land suitable for the supply of condominiums, as noted in last month's monthly report, rising construction costs are said to be a major factor. This is due to a significant rise in resource prices, a global shortage of semiconductors and a shortage of essential housing equipment. The fact that Japan, which relies on imports for many of these goods, is also undergoing a depreciation of the yen, which is also adding to the rise in prices.

This is reflected in the fact that the construction cost index net construction cost of reinforced concrete (RC) for apartment buildings has continued to rise from March to July 2022 to 130.3, 131.5, 132.8, 135.2 and 135.3 respectively, according to the Construction Price Survey Institute.

【3.Information on Property Market Trends: Economic Outlook】

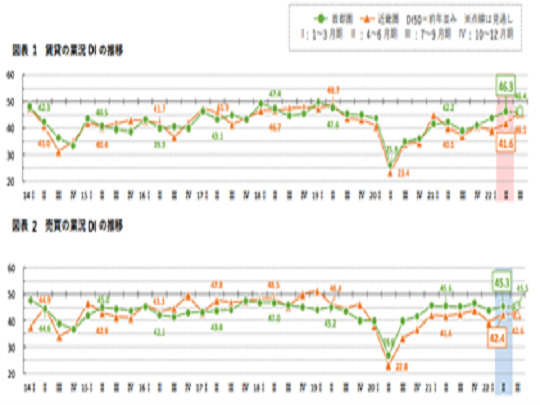

Figure 1 Index of business conditions in the Tokyo and Kinki regions (business conditions DI* Y-o-Y)

(Source: Cited from At Home Co.,Ltd. )

Charts 1 and 2 show business conditions in the local real estate brokerage industry in the period April-June 2022, as published by At Home Co.,Ltd. on 24 August 2022. This is a quarterly survey conducted and published by real estate information service At Home Co.,Ltd. on economic trends in the residential property distribution market in 14 areas in 13 prefectures across Japan, targeting At Home member real estate agencies. The DI used here is an abbreviation for Diffusion Index, an indicator used to measure the direction of business confidence and business sentiment, and is also used to forecast the future of the economy, etc. As shown in Chart 1, the rental DI for the Tokyo metropolitan area is expected to be above 50, while the DI for the Tokyo metropolitan area is expected to be below 50 in the third quarter of 2021. The rental DI in Chart 1 shows that in the Tokyo metropolitan area, the DI has risen for five consecutive quarters since approximately 40 points in the third quarter of 2021, and the range of increase can be confirmed as six points or more. On the other hand, the sales DI in Chart 2 has been on an upward trend since the first quarter of 2022, but has hardly risen from an approximate 45 points, reaching only 45.5 points in the latest third quarter. In other words, the DI for business conditions in the rental brokerage sector has generally shown a steady recovery, particularly in the metropolitan area, as restrictions on movements have eased. However, the DI for business conditions in the sales brokerage sector was negative YoY in 10 of the 14 regions surveyed, reflecting the fact that sales and purchases have been significantly affected by the sharp rise in housing prices and materials.

According to At Home, in areas where business is booming, the easing of the entry restrictions on the new Covid has led to an increase in demand from overseas investors, while in Shinjuku, Tokyo, the company reports that the easing of anti-Covid restrictions has led to a recovery in business conditions, as evidenced by the fact that "the easing of restrictions has also led to increased room search activity, and properties that were not settled during the peak season from January to March are now under contract (Shinjuku Ward, Tokyo)". The report also notes a recovery trend following the easing of restrictions on covid measures. Also, "Family-type flats for rent are firm in line with the rise in condominium sales prices (Suginami Ward, Tokyo)" and "People who are considering purchasing apartments are flowing into the rental sector (Nagoya City, Aichi Prefecture)", indicating that some couples and families are flowing into the rental sector as the price of properties for sale soars.

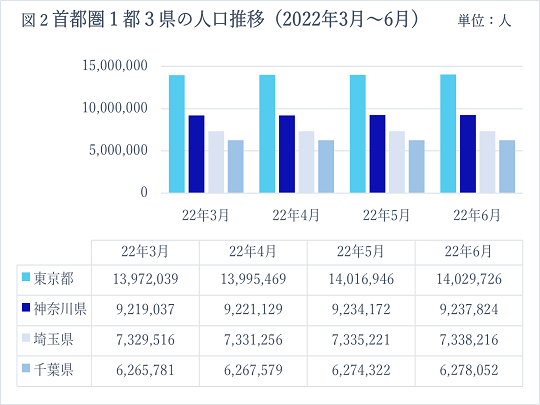

(Source: Compiled by the author based on demographic data from the Tokyo, Kanagawa, Saitama and Chiba city governments / as of 27 August 2021).

Figure 1 shows the population trends in the Tokyo metropolitan area and the three prefectures over the past four months. It shows that Tokyo, Kanagawa, Saitama and Chiba prefectures have all seen their populations continue to expand over the past four months. Although the July edition of this report confirmed the recent downward trend in the population following the spread of the new covid pandemic, four months of continuous population growth suggests a stable recovery in Tokyo and the three prefectures, which is expected to stimulate economic activity in the future.

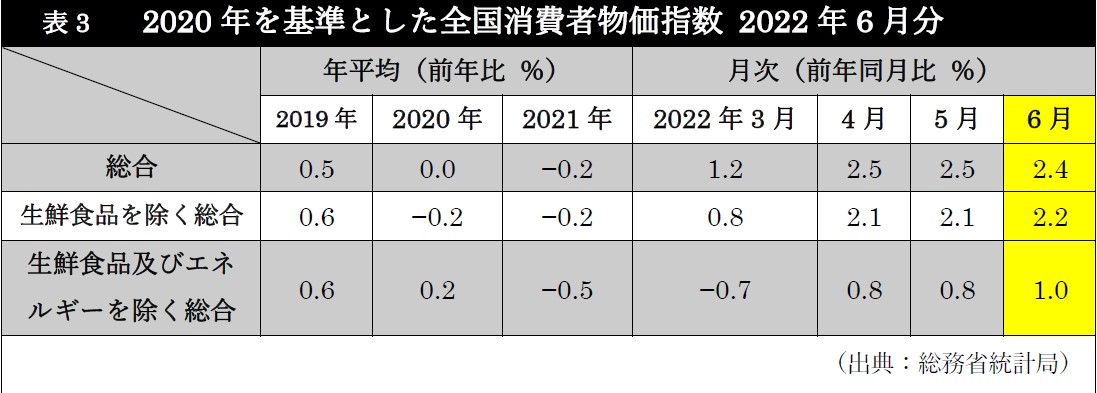

The overall consumption trend is 0.1% lower than last month, but the composite excluding fresh food has increased by 0.1%, while the composite excluding fresh food and energy has increased by 0.2%. The index excluding fresh food, which is the main inflationary factor, and the energy industry, which has shown a more positive trend than in the past, indicate that consumer confidence is on an expansionary trend. As confirmed at the beginning of this report, since the second Kishida cabinet was formed, the Government of Japan has taken further measures against the spread of the new covid infection and has stated that it will " drastically strengthen investment in human resources", thus making further expansion and a recovery in the economy much more likely.

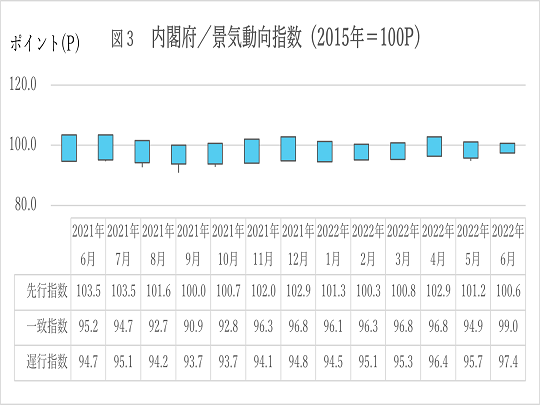

Figure 3, Cabinet Office Economic Outlook Index, shows that, firstly, the leading index fell for the second month in a row, down -0.6 points compared to the previous month. This was the first fall in three months, with the three-month backward moving average (the high and low values obtained by comparing the figures for the month under study with the averages for March, April and May and for April, May and June) falling by 0.06 points, and the seven-month backward moving average (the figures for the month under study with the averages for November, December, January, February, March, April and May and for December, January, February, March, April, May and June) falling by 0.06 points. The seven-month backward moving average (the high/low value calculated by comparing the value for the surveyed month with the average for November, December, January, February, March, April and May and the average for December, January, February, April, May and June) fell 0.20 points, the first fall in three months.

In the coincident index, the index increased by 4.1 points compared to the previous month, which is the first increase in three months. The three-month backward moving average rose by 0.73 points, the first increase in two months, while the seven-month backward moving average rose by 0.38 points, the eighth consecutive monthly increase.

In the lagging index, the index rose by 1.7 points compared to the previous month, the first increase in two months; the three-month backward moving average rose by 0.70 points, the seventh consecutive monthly increase; the seven-month backward moving average rose by 0.47 points, the fourth consecutive monthly increase; and the seven-month forward moving average rose by 0.38 points, the fourth consecutive monthly increase.

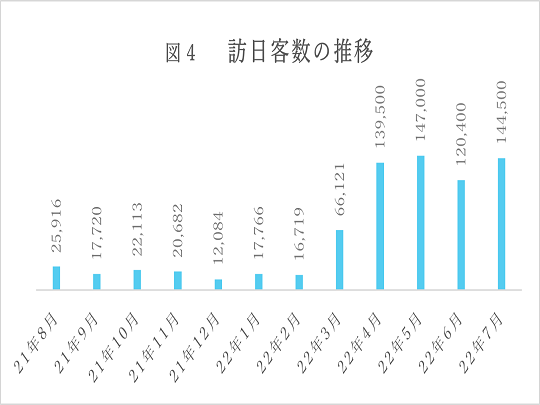

(Source: Japan National Tourist Organisation)

The number of foreign visitors exceeded 100,000 for the fourth consecutive month, partly due to the resumption of new entries for non-tourist purposes under certain conditions from March 2022 and the acceptance of escorted package tours for tourists that began in June. However, the number of visitors decreased by 95.2% to 144,500 compared to the same month of 2019 before the spread of the new corona due to the impact of entry restrictions such as group tours only and the somewhat complicated entry procedures compared to other countries, as can be seen from Fig. 4. The Japanese Government is planning to exempt Japanese citizens from the PCR test before entering Japan from 7 September 2022 on the condition that they have received three doses of the vaccine.

【4.Prospects for Future Property Purchases】

As pointed out at the beginning of this report, there are concerns about stagflation in Japan at present, but the government should try to avoid stagflation by focusing on "investment in people" as a key policy for the "new capitalism" that the reshuffled cabinet is aiming for. With the yen weakening by 24% YoY to 136.72 yen against the US dollar as of 26 August (110 yen the same day last year), property purchases have been boosted. (In its Economic Outlook Index released on 5 July 2022, Teikoku Databank Ltd. reported that business conditions in the real estate industry have improved for four consecutive months. It said that building transactions have remained steady as "property sales prices are not falling due to a shortage of goods". Also, while the report introduces the voice of real estate agents and brokers as 'foreign capital is flowing into real estate investment due to the weak yen and further investment is expected to increase', there were also some harsh comments such as 'the occupancy rate of rental meeting rooms has not fully returned to 2019 levels'.