Q2(Jul – Sep 2022)real GDP growth rate (2nd preliminary seasonally adjusted series values):-0.2% YoY

Q2 real GDP (2nd preliminary values):135 trillion236.2 billion JPY/1.5% YoY

Happy New Year and welcome to the first MARE Monthly Real Estate Market Report of 2023, which is divided into the following chapters: 1. Economic Policies of the Kishida Administration; 2. Property Market Related Information: Basic Data on a Real Economy; 3. Information on Property Market Trends: Economic Outlook; and 4. Prospects for Future Property Purchases. Of the above, in section 1 we will review the difficulties related to real estate during 2023.

We hope that this will help the reader to understand the opportunities for buying or selling property.

【1.Government Policies to Foster an 'Investment in People' Approach】

Three major events are likely to affect the property market this year. Firstly, there is the expectation that the Bank of Japan may raise interest rates around April, when the new Governor takes office. The impact of this can be gauged from the fact that the yen appreciated by about ¥10 last month as a result of a slight increase in the allowable rate of change in long term interest rates. Second, real estate inventories, mainly of existing condominiums, are on the rise. The fact that the number of contracts has been decreasing due to uncertainty about the future of the property market, and that property inventories in the Tokyo metropolitan area have increased as a result, is noteworthy as a possible influence on the future property market. Third, there is a stabilising trend in resource prices: the highest price for WTI crude oil was USD 120 on 6 June, and the latest price was USD 75 on 2 January, indicating a downward trend. Nevertheless, it is still higher than its pre-Covid level and should continue to swing higher and lower depending on the situation in Europe, but with central banks around the world stepping up monetary tightening measures, it is highly unlikely that the price will rise above USD 100 again this year. On the other hand, geopolitical risks in oil-producing countries and a decline in investment in oil exploration related facilities would likely lead to higher energy prices.

The following is a report on the 16th meeting of the Council on Economic and Fiscal Policy held at the Prime Minister's Office on 22 December and the press conference on the results of the meeting to ascertain what policies Prime Minister Kishida is planning with these concerns for the coming new year in view.

Firstly, the Kishida Cabinet states that, although the global economy is expected to slow down in FY2023, the 'Comprehensive Economic Measures to Overcome High Prices and Realise Economic Revival' will function in a full-scale manner and 'investment in people' and investment in growth areas under public-private partnerships will be promoted, so that the economy will be led by private demand at around 1.5% in real terms and 2.1% in nominal terms. Among other things, as a result of comprehensive economic measures based on public-private partnership investment, private investment will be promoted and is forecast to increase by around 5.0% compared to the previous year. Industrial production is also expected to increase by around 2.3% year-on-year in line with the recovery in domestic demand. The number of employed persons is also expected to increase by around 0.2% year-on-year, and the unemployment rate will fall to around 2.4%. Real gross national income (real GNI), the key element of the Kishida Government's 'new capitalism', is expected to increase by around 1.8% year-on-year, exceeding the real GDP growth rate, due to an increase in income associated with growth in business outside Japan and increased investment in Japan. The question is: what has been the actual state of the economy so far? This will be reviewed in the following sections.

【2.Property Market Related Information: Basic Data on a Real Economy】

This section reviews basic real economy information hereafter.

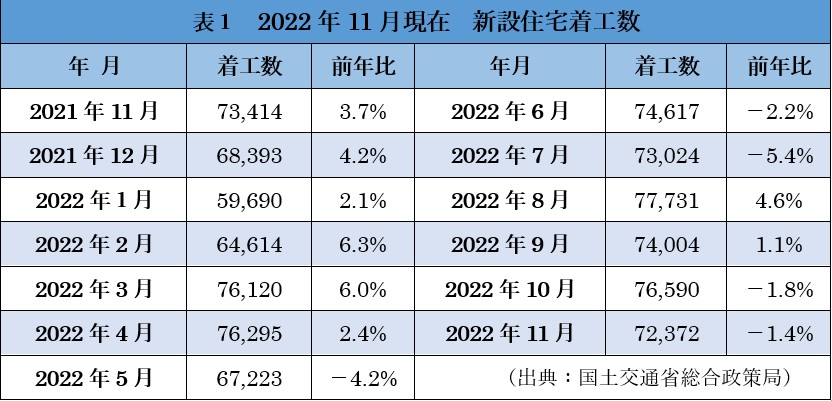

Table 1 shows that new housing starts fell by 4,218 units month-on-month (MoM) and by 1.4% year-on-year to 72,372, indicating a decrease both MoM and YoY. The breakdown is 21,511 owner-occupied units, down 15.1% YoY, showing a decline for the 12th consecutive month, while 29,873 houses for rent increased for the 21st consecutive month, up 11.4% YoY. Houses for sale were 20,642, down 0.8% YoY, indicating a decline for the first time in four months. Owner-occupied dwellings decreased, as both private and public funds decreased. The number of houses for rent increased overall due to an increase in both private and public funding. In the case of houses for sale, both condominiums and detached houses decreased, resulting in an overall decrease in the number of houses for sale. Data released in November by Sanko Estate Co. shows that the vacancy rate in the five central wards of Tokyo (Chiyoda, Chuo, Minato, Shinjuku and Shibuya wards) fell 0.25% MoM to 4.32%, confirming a decline for the third consecutive month. (According to forecasts by the Office Building Research Institute Ltd, demand will continue to far outstrip supply, with a value of 2.5% approaching the pre-Covid level around the third quarter of 2025, and a gradual decline is expected in the future.

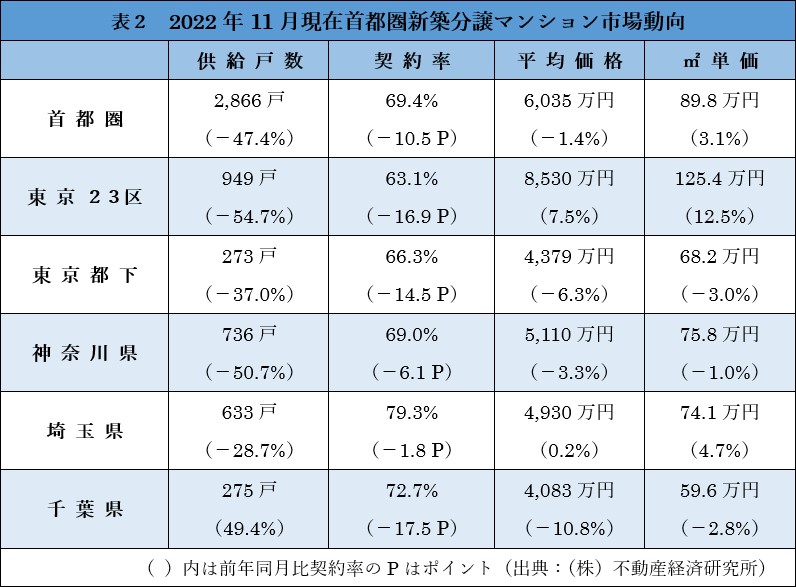

Meanwhile, Table 2, New condominium for sale market trends limited to Tokyo and the three prefectures, shows a 47.4% decrease in the number of units supplied.

As confirmed in the previous month's issue, the sale of large properties in November last year is expected to be a major factor in this result, with the number of remaining units increasing by 134 units from 4,945 last month to 5,079 this time. The number of units supplied fell in all regions except Chiba Prefecture, where the contract rate was negative in all areas. The average sales price and unit price per square metre remained largely unchanged, but the contract rate for super high-rise properties with 20 or more floors was 65.9%, the lowest level since January 2022. The number of units put on sale fell for the second consecutive month to 1,128 units, down 14.9% YoY. The first month contract rate was 58.4%, the first time since September 2021 that the rate had fallen below 70%. Meanwhile, the average price was JPY 61.57 million and the price per m2 was JPY 947,000, showing an increase for the first time in three months.

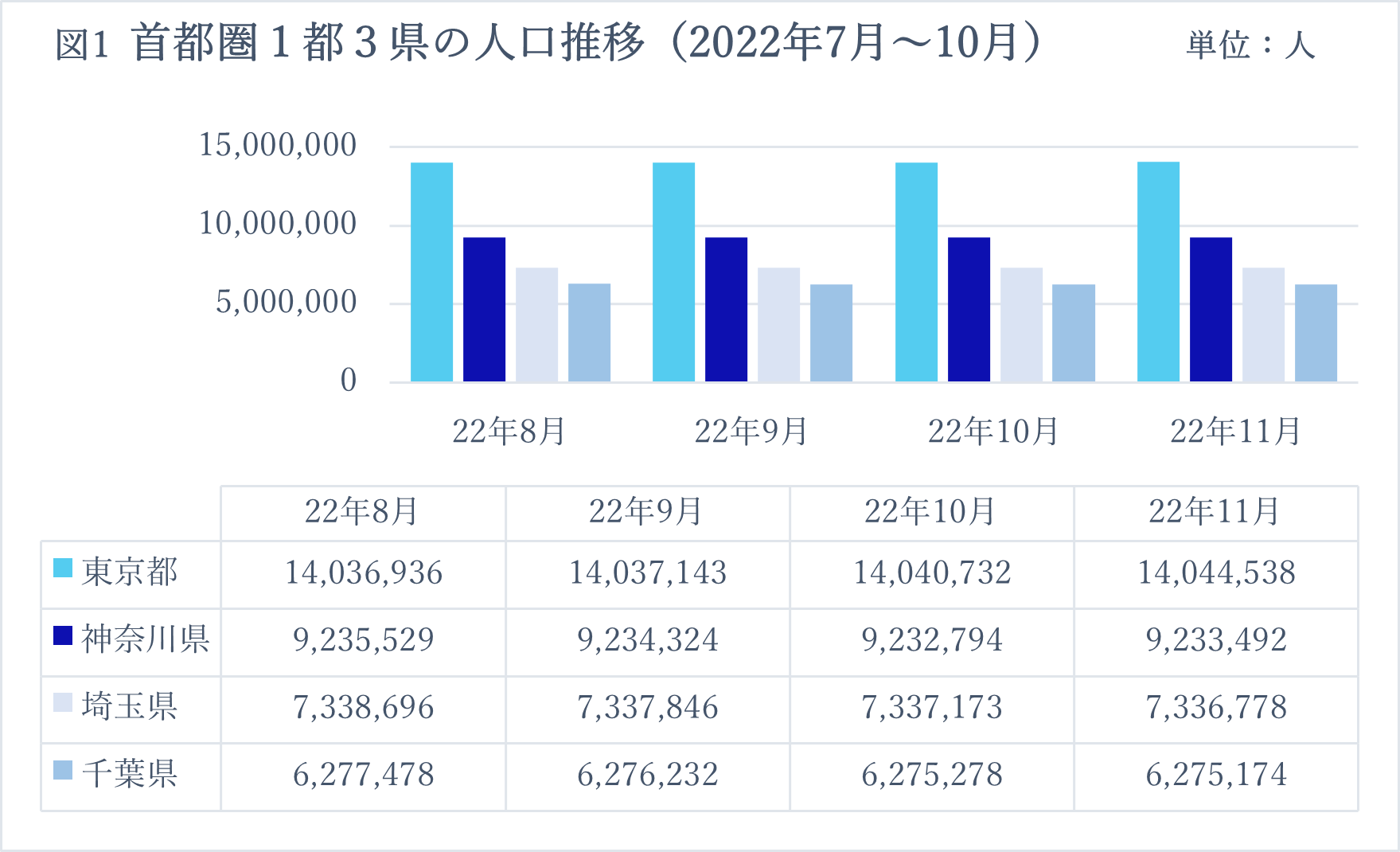

(Source: Compiled by the author based on demographic data from the Tokyo, Kanagawa, Saitama and Chiba city governments / as of 7 January 2023).

In terms of population change, Tokyo showed an increase of 3,806 persons, an increase for the eighth consecutive month, while Kanagawa Prefecture also showed an increase for the first time in June 2022, with an increase of 698 persons. On the other hand, the other two prefectures showed a decrease. Looking limited to the prefectures that experienced a decline, the population decreased by 3,157 persons in the October quarter, but by 499 persons in the November quarter, a relatively subdued decline compared to the previous years. Tokyo, which also saw 3,589 people move into the city in the October quarter, saw a further increase in the November quarter, with 3,806 people moving into the city, continuing the trend of outstandingly large increases in Tokyo. As in the previous month, it is expected that, as the situation of the Covid has settled down, the so-called 'Covid evacuees' who had temporarily moved from the cities to the countryside have returned one after the other.

【3.Information on Property Market Trends: Economic Outlook】

In this section, the business climate pertaining to the property market is reviewed. Start by checking the macroscale data.

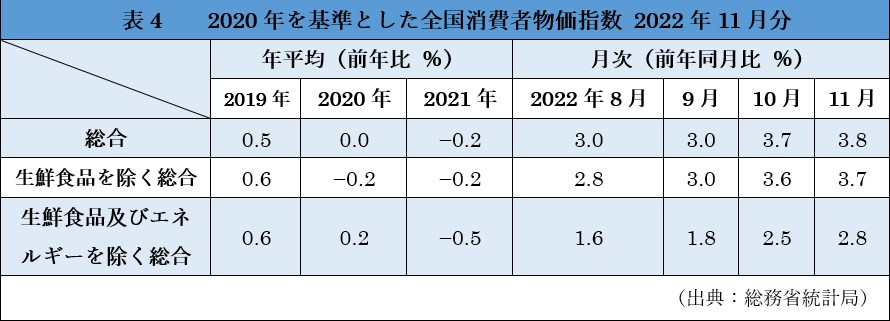

Table 4, National Consumer Price Index, shows that the composite value increased by 0.1% from last month to 3.8%, with the composite excluding fresh food increasing by 0.1% to 3.7% and the composite excluding fresh food and energy by 0.3% to 2.8%. The 3.7% YoY rise in the composite excluding fresh food was the highest level in 40 years and 11 months since December 1981, following the second oil crisis triggered by the sharp decline in oil production following the Iranian Revolution. In response, on 2 December 2022, the Government passed the second supplementary budget for fiscal year 2022, with a budget of 7.8 trillion yen as a countermeasure against price hikes. If these government policies, in addition to the global economic situation described at the beginning of this article, are successful, we can expect a gradual decline in price rises from this year.

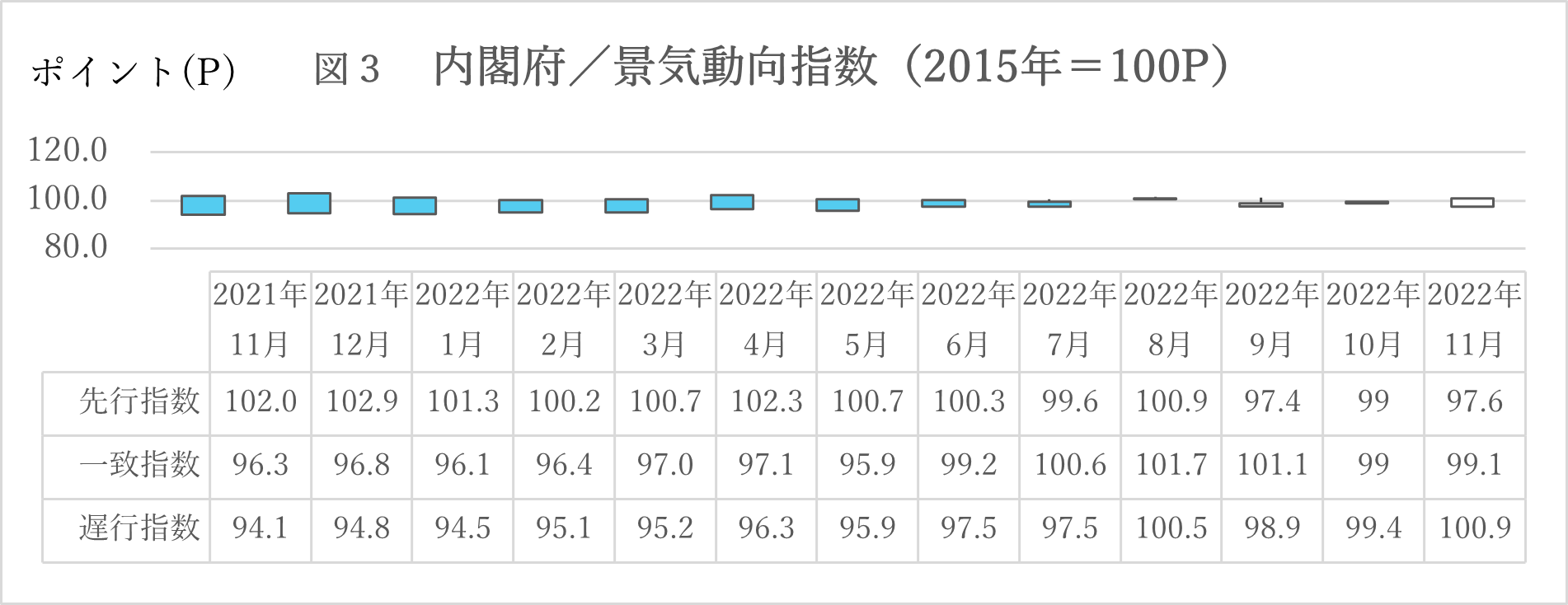

According to Figure 3, the Cabinet Office Economic Climate Index, the Leading Index fell 1.0 point ("P") from the previous month, the first fall in two months; the 3-month backward moving average (the high and low values obtained by comparing the figures for the month under study with the averages for August, September and October and for September, October and November) fell 1.34 P, the third consecutive monthly fall; and the 7-month backward moving average (the figures for the month under study compared with the averages for April, May, May, June, July, August, September, October and November) fell 1.35 P, the third consecutive monthly fall. The seven-month backward moving average (the high/low value calculated by comparing the figure for the month under study with the average for April, May, June, July, August, September and October and the average for May, June, July, August, September, October and November) fell by 0.69 P, the third consecutive monthly fall.

The Consistent Index fell by 0.5P MoM, the third consecutive monthly decline; the 3-month backward moving average fell by 0.74P, the second consecutive monthly decline; the 7-month backward moving average rose by 0.30P, the 13th consecutive monthly increase; the 7-month backward moving average rose by 0.30P, the 12th consecutive monthly increase; and the 3-month backward moving average fell by 0.74P, the 12th consecutive month of decline.

The Lagging Index increased by 1.7P MoM, rising for the fourth consecutive month; the 3-month backward moving average increased by 0.73P, rising for the twelfth consecutive month; the 7-month backward moving average increased by 0.66P, rising for the ninth consecutive month; and the 7-month forward and coincident indexes increased by 1.7P, rising for the thirteenth consecutive month.

The Leading and Consistent Indexes decreased, while the Lagging Index showed an increase. The following section provides breakdown information showing a downward trend compared to the previous month. The index of inventories of final demand goods decreased by 0.49%, the index of inventories of essential industrial goods decreased by 0.04%, the floor area of new housing starts decreased by 0.24%, the consumer attitude index decreased by 0.47% and the outlook for small business sales also showed a decrease of 0.42%. Meanwhile, the number of new job openings rose by 0.38% and the TSE Stock Price Index showed an increase of 0.24%. In terms of matching indices, the Investment Materials Shipment Index decreased by 0.30%, Commercial Sales (Retail) decreased by 0.21% and Commercial Sales (Wholesale) decreased by 0.15%. In contrast, the index for durable goods shipments rose by 0.41%. Lagging Index showed notable increases, with corporate tax revenues rising by 1.18%, the unemployment rate improving by 0.25%, the consumer price index rising by 0.15% and the index of inventories of final demand goods rising by 0.17%. In general, the Cabinet Office states that business confidence is improving overall, as the seven-month backward moving average in the Consistent Index has risen continuously.

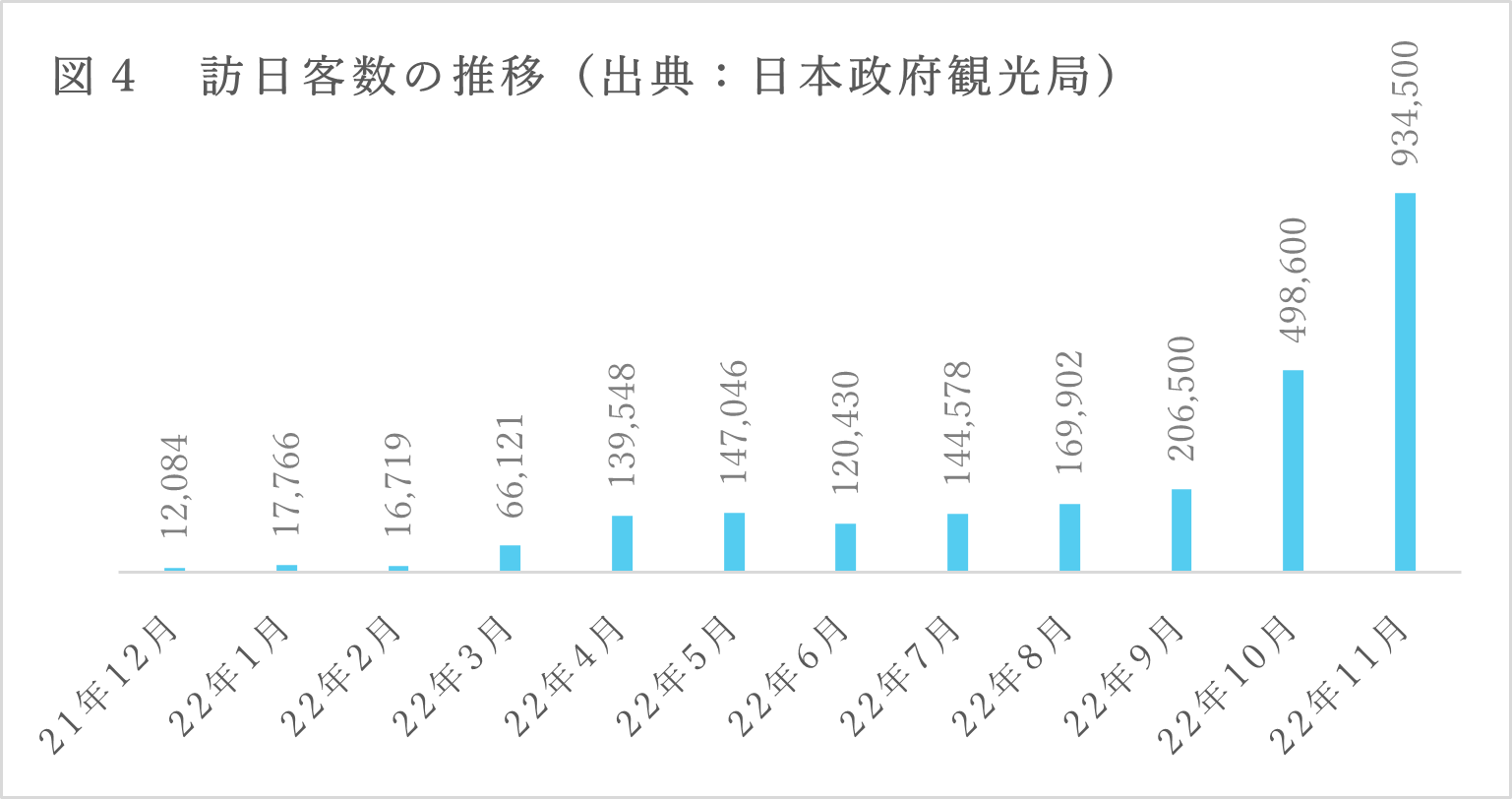

Figure 4 shows the number of visitors to Japan up to November last year. According to a press release by the Japan National Tourist Organisation dated 21 December 2022, the number of visitors has recovered to nearly 40% of the pre-Covid level for the same month in 2019, due to the Japanese Government's implementation of measures such as the acceptance of individual travel and the resumption of visa waiver measures from October. In particular, the significant increase in the number of tourists from the East Asian region was a boosting factor. In addition, air traffic has increased, but not to the pre-Covid level, and there is plenty of room for further growth in the number of visitors in the future, given the positioning of tourism as a key element of the policy.

【4.Prospects for Future Property Purchases】

Looking at exchange rate trends, the yen continued to appreciate to 133.64 yen as of 6 January this year (116.04 yen the same day last year), but compared to the same day last year, the yen has depreciated by about 13%, which means that the yen is still weaker than in the past. The Kishida Government, which is aiming for economic growth and higher wages by making effective use of the 'cheap yen', can easily be assumed to be averse to further yen appreciation, but the possibility of further yen appreciation in the future cannot be ruled out, depending on the future direction of inbound demand, which will continue to increase, and the interest rates policy of the Bank of Japan. According to the Teikoku Databank TDB Business Trend Survey (nationwide), the current situation in the real estate industry is such that "property prices are stable at high levels and transactions are brisk" and "customers are not keeping up with the situation due to soaring construction costs and rising land prices", both of which are backward looking. There are also concerns about the outlook for the future, with positive sentiments such as 'the rush to build condominiums for sale is expected to calm down in a year's time' and 'young people are expected to continue investing in property and real estate is expected to become a source of unearned income', as well as 'interest rates will enter an upward phase from April 2023 onwards and mortgage rates will rise'. According to the Monthly Survey of Labour Statistics (preliminary report for November 2022) published by the Ministry of Health, Labour and Welfare, real wages per worker at establishments with five or more employees decreased by 3.8% YoY. Despite the Government's flagship policy of 'investment in people', which was also confirmed in [1] of this report, wage increases by companies have not kept pace with price increases, and real wages have been lower than in the same month of the previous year for eight consecutive months. In view of the above, it can be predicted that the recent property market, which has continued to appreciate, will gradually collapse in value. However, by assessing the attractiveness of individual properties, properties in unique conditions can be of good one. The value of such properties will continue to rise. This trend is also increasing, and the importance of reliable real estate agencies with a good eye for such properties is growing.