Q2(Jul – Sep 2022)real GDP growth rate (1st preliminary seasonally adjusted series values): 0.2% YoY

Q3 real GDP (1st preliminary values):140 trillion178billionJPY/0.6% YoY (Source:Cabinet Office)

The February 2023 edition of the MARE Monthly Real Estate Market Report will be divided into the following chapters.

1. Economic Policies of the Kishida Administration; 2. Property Market Related Information: Basic Data on a Real Economy; 3. Information on Property Market Trends: Economic Outlook; and 4. Prospects for Future Property Purchases. Of the above, in section 1. I will review the difficulties related to real estate during 2023.

I hope that this will help our readers to understand the opportunities for buying or selling property.

【1.Government Policies to Foster an 'Investment in People' Approach】

On last month's issue, I noted three major events that are likely to affect the property market. More than a month has passed since that date and I would like to share our thoughts on the current situation. First, regarding the forecast of an interest rate hike following the appointment of the new BOJ governor in April this year. On 14 February, the Government of Japan submitted a proposal to the Governing Council of the House of Representatives and the House of Councillors for appointing Kazuo Ueda as the Bank of Japan Governor for the succeeding period. Given that Mr.Ueda has spoken of continued monetary easing, a sudden change in policy is difficult to predict and therefore yen appreciation is likely to be postponed. Second, regarding the upward trend in property inventories. This trend is likely to continue for some time, with a month-on-month increase of 840 units remaining as of December last year. However, as the supply of new condominiums for sale is declining, the current size of the market will not directly lead to a price collapse in the property market. Third, regarding the stabilising trend in resource prices. This is the most likely factor for a possible recession: after reaching a peak of USD 120 on 6 June, WTI crude oil has stabilised over the past few months at USD 76 as recently as 17 February. However, oil prices are likely to rise in the coming months as the Chinese economy, which has emerged from its zero-covid policy, shows a faster than expected revival, predicts Goldman Sachs, the largest investment bank in the United States.

The following section will examine Prime Minister Kishida's policy plans bearing in mind these New Year concerns, from the first and second meetings of the Economic and Fiscal Advisory Council in 2023 held at the Prime Minister's Office on 16 and 24 January, as well as the press conference on the results of these meetings.

In the midst of drastic changes in the economic situation and social environment in the world, the Government aims to manage the economy in a well-prepared manner so as to quickly implement comprehensive economic measures, supplementary budgets and measures to realise "the new capitalism" and restore economy to a private demand-led economic growth path. The Government intends to support the realisation of sustainable wage growth, which is at the core of this, by strengthening investment in innovation and people, while helping to secure resources for wage increases through appropriate pricing. In addition, in order to build a resilient Japanese economy at the macroscopic level as well, the government has presented a picture of the primary budget balance for the national and local governments combined to return to surplus by FY2025, in order to strengthen "the new capitalism" and lead international policy trends, while realising a virtuous cycle of growth and distribution.

In addition, with the aim to nurture the future generation that will sustain the rich Japanese market, a Child and Family Agency will be established in April this year, with plans to present a general framework for doubling the future budget for children by June.

According to the preliminary December Monthly Survey of Labour Statistics released by the Ministry of Health, Labour and Welfare on 7 February, total cash salaries (nominal wages) excluding the effect of prices increased by 4.8% YoY, while real wages, including the effect of rising prices, rose by 0.1% YoY. Although this is the first increase in nine months, the effect of the wage increase still cannot be seen to have been realised, as the increase in wages within the fixed salary range, which shows the underlying tone of wages, was only 1.8% YoY. It will take time for the rate of inflation to fall below the rate of wage increase, but the author predicts that, with the Government's efforts to prepare various policies for price stability and the results of the annual spring wage negotiations (Shunto), the rate of wage increase would exceed the rate of inflation price by the end of the year.

In the following section, the economic realities surrounding the property market are reviewed.

【2.Property Market Related Information: Basic Data on a Real Economy】

This section reviews basic real economy information.

Table 1 shows that new housing starts fell by 5,123 units MoM and by 1.7% YoY to 67,249, marking the third consecutive month of decline. The number of owner-occupied dwellings was 19,768, down 13.0% YoY and marking the 13th consecutive month of decline, while the number of houses for rent was 26,845, up 6.4% YoY and marking the 22nd consecutive month of increase. In addition, the number of houses for sale increased by 1.4% YoY to 20,200 units, turning to an increase after four consecutive months of decline. The number of owner-occupied dwellings decreased overall, as both private and public funds decreased. The number of houses for rent increased overall due to an increase in both private and public funds. In the condominium sales sector, condominiums increased, while detached houses decreased, showing a clear division between condominiums and detached houses. According to December data from Sanko Estate Co, the vacancy rate for large rental office buildings in the five central wards of Tokyo (Chiyoda, Chuo, Minato, Shinjuku and Shibuya wards) was 4.15%, down 0.17% on the previous month, confirming a fourth consecutive monthly decline. The vacancy rate for medium-sized rental office buildings fell for the second month in a row to 6.79%, while the overall average was 4.82%, showing a decline for the fourth consecutive month. The company's Office Building Research Institute forecasts that demand will continue to significantly outstrip supply, so that a value of 2.5%, approaching pre-Covid levels, will be reached around the third quarter of 2025, and a gradual decline is expected to continue.

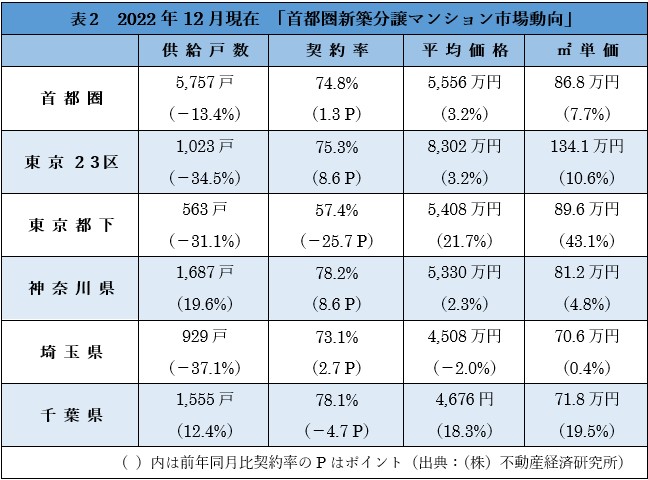

Table 2, New Condominiums for Sale Market Trends, limited to Tokyo and the three prefectures, shows a 13.4% decrease in the number of units supplied. As confirmed in the previous month's issue, the number of units remaining increased by 840 units from 5,079 last month to 5,919 this time, although it is expected that the sale of large properties in November last year was also largely reflected in this result. The number of units on sale fell for the third consecutive month, by 13.4% YoY to 892 units. The number of units supplied fell in all regions except Kanagawa and Chiba prefectures, while the contract rate was negative only in Tokyo suburbs and Chiba prefecture. The average sales price and unit price per square metre each increased slightly, and the contract rate for high-rise properties with 20 or more levels reached 90.5%, the highest level since December last year, but this is likely to have been largely due to year-end sales and bonuses. As for the first month contract rate, 74.8% is indicated, marking the first time in two months that the rate has been above 70%. Meanwhile, the average price per unit was 55.56 million JPY and the average price per square metre was 0.868 million JPY, rising for the second consecutive month.

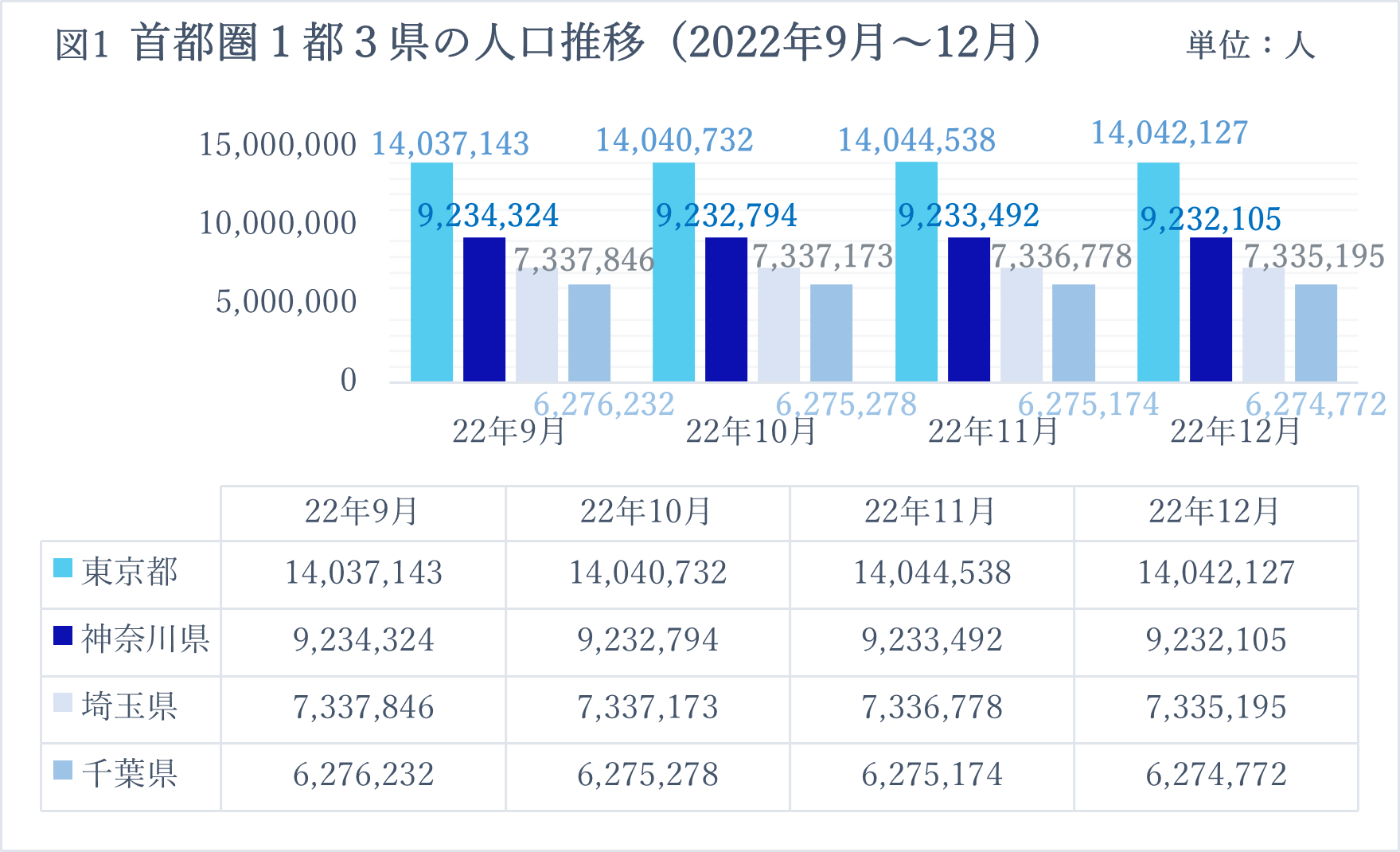

(Source: Compiled by the author based on demographic data from the Tokyo, Kanagawa, Saitama and Chiba city governments / as of 16 February 2023).

In terms of population change, Tokyo showed the first decline in population in nine months, with a fall of 2,411 people, while the population also decreased in the other three prefectures. In December 2022, all three prefectures experienced an excess of outgoing migration, particularly in Tokyo, for the first time since February 2022. As the Covid pandemic subsides and more people return to office work from remote locations, the reasons for the decline in Tokyo's population are not clear, but the author believes that the increasing trend of overseas migrants is an important contributing factor as well. According to statistics from the Ministry of Foreign Affairs' survey of the Number of Japanese Residents Abroad, the total number of permanent residents who moved their place of residence from Japan to overseas reached a record high of approximately 557,000 as of 1 October last year, with the number of permanent residents increasing by approximately 20,000 YoY. These expatriates are likely to want to sell their homes, which the author believes could be a factor in increasing the number of existing properties on the market in the foreseeable future. This trend is expected to continue to increase in the future, but as it is a gradual upward trend, it does not seem to be a factor that will dramatically reduce the population of Tokyo in the long term. Although the Government continues to provide various subsidies to eliminate the concentration of population in Tokyo, if there is a high concentration of workplaces, it will be difficult to eliminate the problem at an early stage. Therefore, it is expected that the Tokyo population will either remain parallel or continue to rise.

【3.Information on Property Market Trends: Economic Outlook】

In this section, the business climate pertaining to the property market is reviewed. First, macro data will be reviewed.

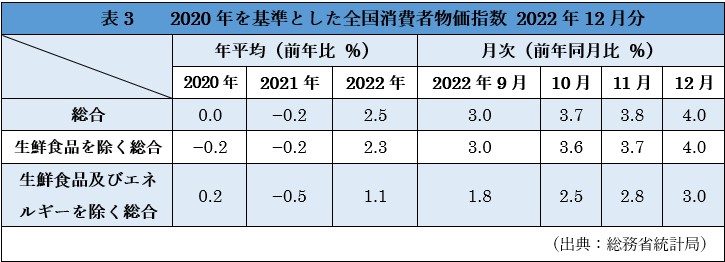

Table 3, National Consumer Price Index, shows that the composite value increased by 0.2% from last month to 4.0%, with the composite excluding fresh food increasing by 0.3% to 4.0% and the composite excluding fresh food and energy increasing by 0.2% to 3.0%. The 4.0% YoY rise in the composite excluding fresh food was the highest since December 1981, following the second oil crisis triggered by the sharp decline in oil production following the Iranian Revolution last month. In response, the Government passed the second supplementary budget for 2022 on 2 December, with a budget of 7.8 trillion JPY as a countermeasure against price soaring. If these government policies, in addition to the global economic situation described at the beginning of this report, are successful, we can expect a gradual decline in price rises from this year. As we have confirmed in previous MARE property market reports, the Government is aware of the importance of wage increases in the context of rising prices, and the foundations are in place for workers to put forward strong demands for higher wages. Therefore, the author believes that there is a very good chance that, during the course of this year, large wage increases will be realised, mainly at large companies, following the spring struggles in which trade unions from various companies submit their demands for wage increases, etc. to their respective companies every spring on a nationwide scale and engage in collective bargaining. This is because there is a general consensus in many sectors that the inflationary trend is likely to continue and that it will be extremely difficult to overcome this trend without a substantial wage increase.

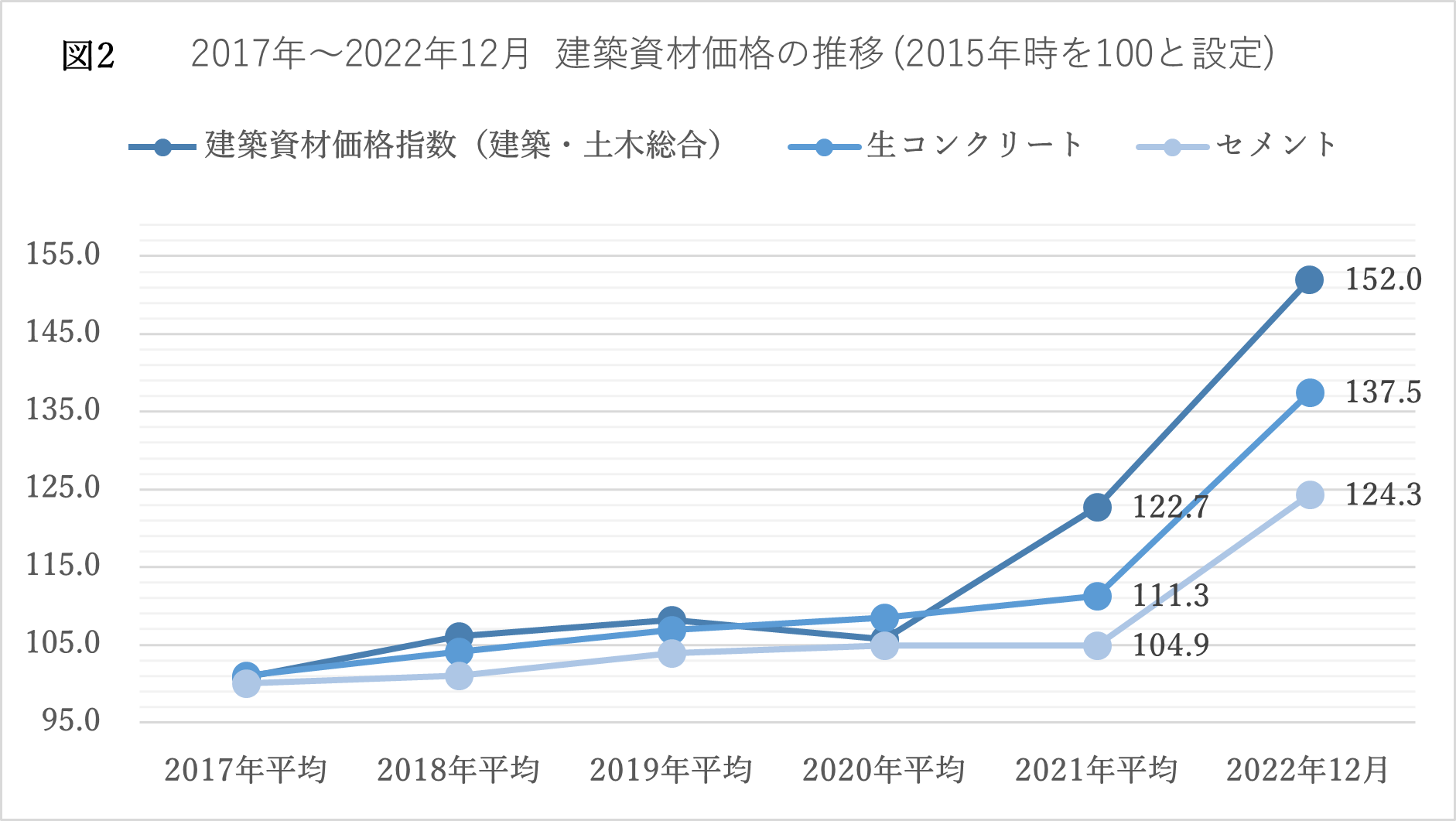

(Source: Compiled by referring to the Economic Research Association's 'Building Materials Price Index').

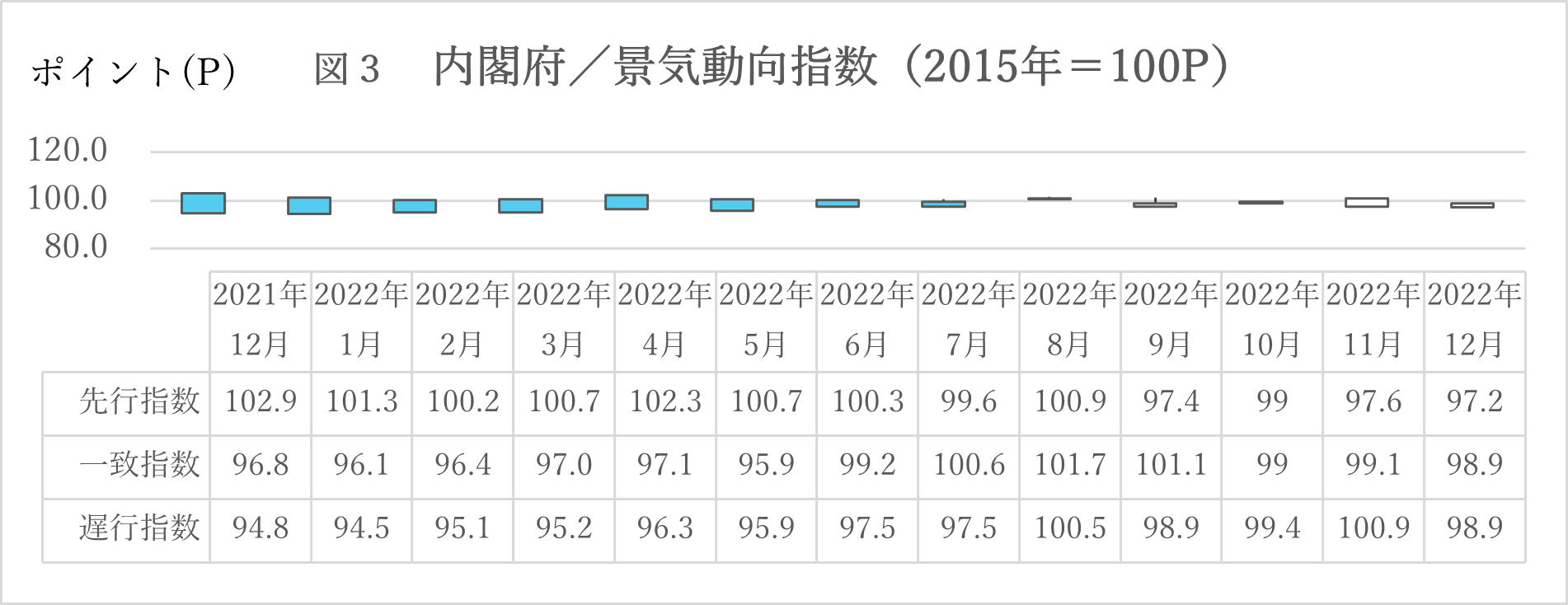

The inflationary situation is well reflected in building materials. Figure 2 shows the Building Materials Price Index, which represents all materials used for construction, and the market prices of ready-mixed concrete and cement, the main types of building material.The average prices from 2017 to 2021 and the prices as of December 2022 are shown, indicating a tremendous increase in prices since the Covid Pandemic. The prices have soared to levels that have never been experienced before. The author expects these price rises to continue this year, and is one of the main reasons for the current high property prices. Perhaps reflecting this situation, recent economic trends appear to be unfavourable. Figure 3 below shows the Cabinet Office's business climate index.

The leading index fell 0.4 points ('P') from the previous month, the second consecutive monthly decline, while the three-month backward moving average (the high/low value calculated by comparing the figures for the month under review with the averages for September, October and November and for October, November and December) fell 0.47 points, the fourth consecutive monthly decline, and the seven-month backward moving average (the high/low value calculated by comparing the figure for the month under study with the average for May, June, July, August, September, October and November and the average for June, July, August, September, October, November and December) fell by 0.51 P, the fourth consecutive monthly fall.

The consistent index fell by 0. 4 P MoM, the fourth consecutive monthly decline; the three-month backward moving average fell by 0. 63 P, the third consecutive monthly decline; the seven-month backward moving average rose by 0. 43 P, the fourteenth consecutive monthly increase; the seven-month backward moving average rose by 0. 12 P MoM, the first monthly decline.

The lagging index rose by 0.9p month-on-month, the first increase in five months; the three-month backward moving average fell by 0.03p, the first decline in 14 months; the seven-month backward moving average rose by 0.44p, the tenth consecutive monthly increase; and the seven-month forward moving average rose by 0.43p, the tenth consecutive monthly increase.

The leading, consistent and lagging indices all showed declines. The following section provides breakdown information on the downward trend compared to the previous month. In the leading indices, the index of inventories of final demand goods decreased by 0.04%, the index of inventories of production goods required by industry decreased by 0.36%, the number of new job openings decreased by 0.23%, new housing starts decreased by 0.07%, the Nikkei Commodity Index (Type 42) decreased by 0.18%, money stocks decreased by 0.17%, the TSE Stock Index decreased by 0.11% and the SME sales outlook showed a decrease of 0.03%. The only index that showed information was the consumer attitude index, which showed an increase of 0.74%. In terms of matching indices, the production index (mining) showed a decrease of 0.01%, the index of shipments of industrial production goods decreased by 0.22%, the labour input index decreased by 0.01%, commercial sales (wholesale) decreased by 0.11% and the export volume index decreased by 0.50%. On the other hand, the consumer durables shipments index rose by 0.23%, the investment materials shipments index (excluding transport machinery) rose by 0.06%, commercial sales (retail trade) rose by 0.15% and the effective job vacancy rate showed an increase of 0.02%. Lagging indices showed a 1.06% decrease in corporate tax revenues and a 0.45% decrease in the final demand goods inventories index. Meanwhile, the unemployment rate improved by 0.10% and the consumer price index showed an increase of 0.55%. As a general comment, the Cabinet Office described business confidence as 'at a standstill'. This is the first time this expression has been used since last February and suggests that the economy may have entered a recessionary phase, so caution should be exercised in future economic phases.

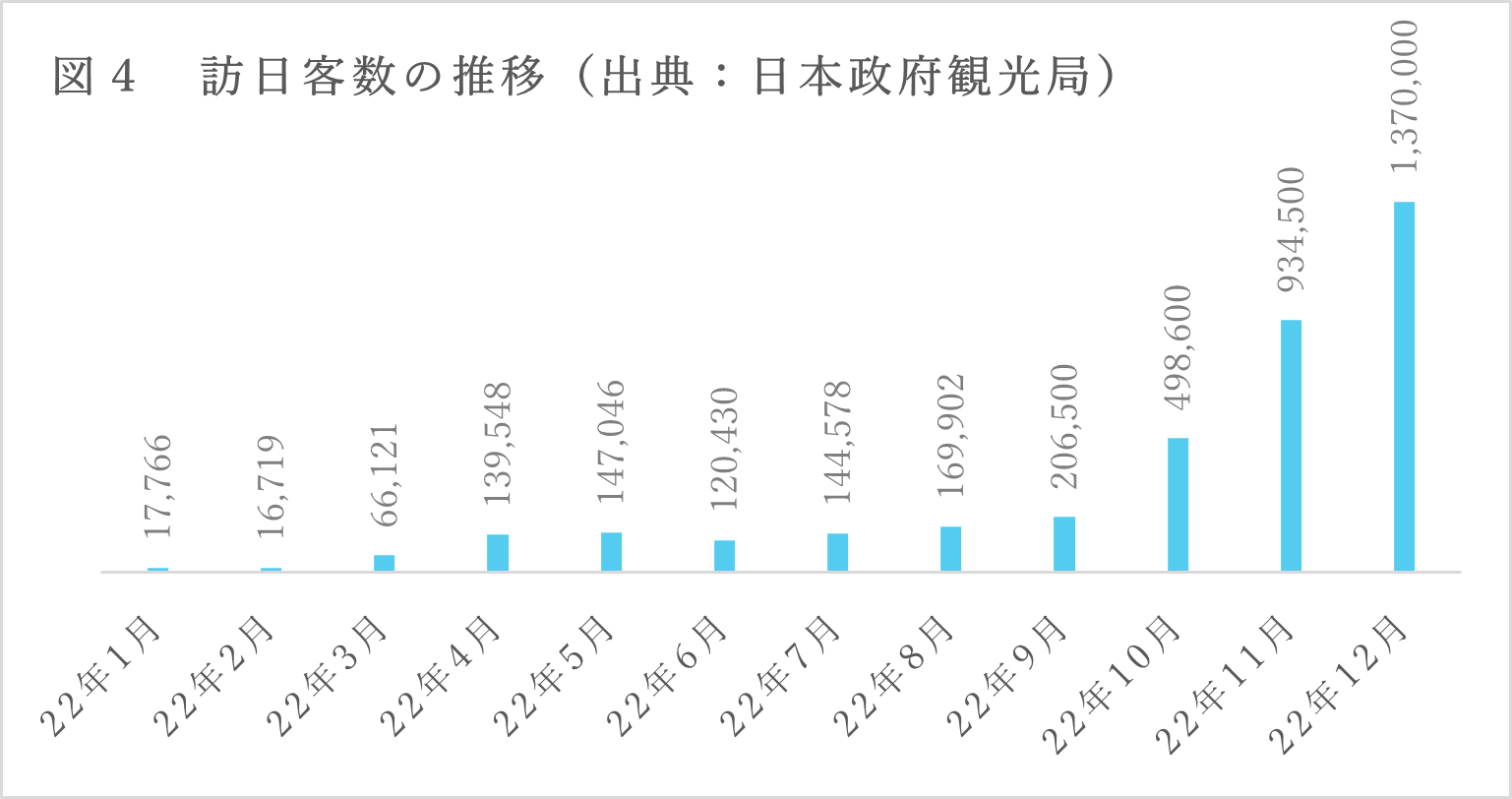

Figure 4 shows the number of visitors to Japan up to December last year. According to data released by the Japan National Tourist Organisation on 18 January 2023, there has been a significant recovery since the implementation of various government measures to ease entry restrictions from October. In particular, the significant increase in the number of tourists from South Korea, Thailand and the USA has been a boosting factor. Air traffic is on the rise, and with tourism positioned as a key policy driver, it is highly likely that the number of visitors will increase further in the future.

【4.Prospects for Future Property Purchases】

Looking at exchange rate trends, the yen continued to appreciate to 132.73 yen as of 15 February this year (115.42 yen the same day last year), but compared to the same day last year, the yen has depreciated by about 15%, which means that the yen is still weaker than before. On 14 February, the Government of Japan presented a proposal to the House of Representatives Steering Committee to appoint Kazuo Ueda as the successor to Bank of Japan Governor Kuroda, whose term of office will expire on 8 April this year. If the procedure goes smoothly, Mr.Ueda will become Governor from 9 April. He is seen as reluctant to end monetary easing or raise interest rates and cautious about long-term government bond yield control (YCC: yield curve control). He has also stated that the current situation requires monetary easing to continue, and therefore, the yen is not expected to show an early appreciation trend. However, in the longer term, an interest rate hike to make up the interest rate gap with the rest of the world, particularly the US, and the removal of the YCC are expected, and if these are implemented, the yen will swing higher. The sustained depreciation of the yen is a positive tailwind for the Kishida Government, which aims to grow by making effective use of the yen's weakness. However, while the market is expecting the implementation of these measures to be delayed for the time being, attention will be focused on his policy statement once he actually assumes the post of governor.

Given this situation, it is a good idea to buy property at a time when the benefits of a weaker yen can be enjoyed.